The E&S insurance market is having a moment. Submission volumes are climbing, new risk categories are entering the market, and carriers, MGAs, and brokers are all competing for the same placements. Everyone is moving faster, or trying to.

The conversation around how to keep up has landed almost entirely on AI. Which model, which vendor, which integration. The assumption is that the right tool will solve the problem, that finding something smart enough will take care of the rest.

What that conversation consistently skips over is the workflow those tools are being dropped into. Despite years of investment in technology, most insurance operations still run on manual intake, inconsistent clearance processes, and data that gets rekeyed by hand before it reaches an underwriter. Adding a point tool to that chain makes one step faster without changing how the operation actually runs.

Underwriting workflow automation addresses a different question entirely, not which tool to add, but how to replace the manual chain from submission inbox to AMS entry with a single, automated pipeline. That’s the real AI opportunity in E&S insurance, and it’s where the competitive gap is starting to open.

The E&S Market Is Growing. The Workflows Aren’t Keeping Up.

The E&S market has grown significantly over the past several years. More risks are being pushed into the non-admitted market as standard carriers tighten appetite. Submission volumes are up across commercial property, casualty, and specialty lines. The pipeline is fuller than it has been in years.

The operational infrastructure handling that volume hasn’t kept pace. Most submission intake still runs through email, with attachments that vary in format, completeness, and quality depending on the broker. Data entry into AMS and PAS systems is still largely manual. Clearance processes vary across teams and branch offices, producing inconsistent results at scale.

The consequence shows up in turnaround times. When intake is manual, processing speed is capped by headcount. During peak periods (renewal seasons, CAT events, sudden market dislocations) the backlog grows faster than teams can work through it. Underwriters end up spending a meaningful portion of their day moving and cleaning data rather than evaluating risk, which is the work that actually drives revenue.

The E&S market rewards speed. The first carrier or MGA to deliver a clean, accurate quote frequently wins the placement. When the intake process creates delays before underwriting even begins, that advantage goes to whoever has found a way to remove the manual bottleneck from the front end of the workflow.

What Most AI Implementations Actually Do

Most carriers, MGAs, and brokers have added at least one AI tool to their operations over the past two years. The pressure to do something with AI has been significant, and the vendor landscape has expanded quickly to meet it.

The typical implementation follows a familiar pattern. A tool gets selected, procurement happens, the tool gets integrated into the existing workflow, and one step in the process gets faster. An OCR tool handles one document type. A chatbot fields broker queries. A single-field extraction tool pulls named insured information from a specific form. Each of these solves a narrow problem reasonably well.

The issue is what happens around those tools. The rest of the workflow, the sorting, the rekeying, the validation, the handoffs between systems, continues as before. The operation looks like it has adopted AI, and in a limited sense it has, but the underlying process hasn’t changed. Data still moves through the same manual steps. Errors still accumulate before anyone catches them. Turnaround times improve marginally on the automated step and stay the same everywhere else.

This is the natural result of point-tool adoption. Each tool is evaluated and purchased to solve a specific problem, which it does. The broader workflow, the chain of steps that connects a submission email to a quote-ready file in the AMS, remains fragmented. And as submission volume grows, the fragmentation compounds rather than resolves.

The conversation about AI in insurance has focused heavily on which tools to adopt. The more useful question for an MGA or carrier trying to scale is what the full workflow looks like after automation, and whether the tools in place are actually connected enough to answer it.

What Underwriting Workflow Automation Actually Means

Underwriting workflow automation is a different proposition from adding tools to an existing process. The goal is replacing the manual chain entirely, connecting every step from submission intake to AMS entry into a single, automated pipeline that runs without human intervention except where judgment is genuinely required.

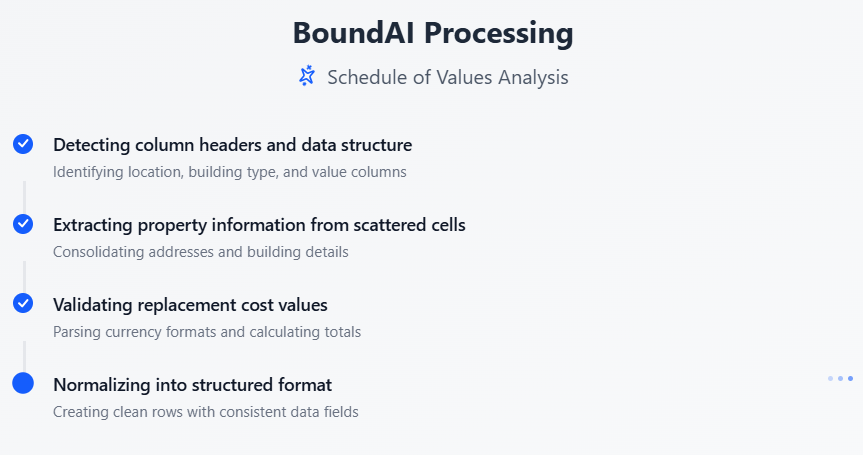

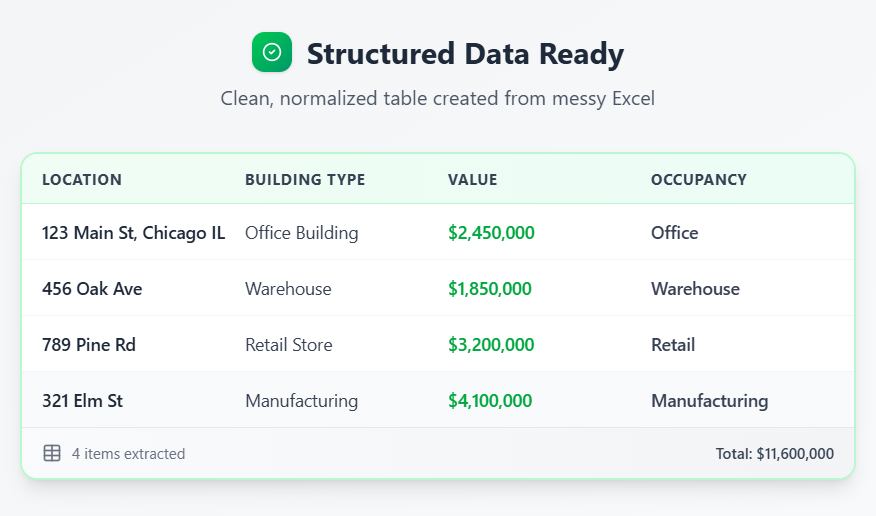

In practice, that pipeline looks like this. A submission arrives in a shared inbox. The system picks it up, identifies every document in the submission, and classifies each one by type, whether that’s an ACORD form, an SOV, a loss run, a supplemental, or an inspection report. From there, relevant data fields are extracted from each document based on what it is, not based on a fixed template that breaks when the format changes.

Extracted data then goes through normalization, converting values into formats the downstream system can accept. Currency figures, date formats, abbreviations, and field names get standardized automatically. Validation runs against expected ranges and formats, flagging anomalies before they enter the system rather than after. Duplicate checks and compliance screening happen in the same pipeline. Once everything clears, structured data writes directly into the AMS or PAS.

Anything the system isn’t confident about gets routed to a human reviewer rather than pushed through automatically. The underwriter opens a file that is already structured, cleared, and ready for assessment.

The difference between this and point-tool automation is the scope of what gets handled. A single tool makes one step faster. Workflow infrastructure removes the manual work from the entire chain. That’s the distinction that matters when submission volume is growing and turnaround time is a competitive variable.

Why E&S and Specialty Lines Are the Right Place to Start

Workflow automation delivers value across insurance lines, but the return is highest in E&S and specialty lines, and the reason comes down to document complexity.

Standard market submissions follow relatively predictable structures. ACORD forms are standard. Brokers work within established templates. The document landscape is consistent enough that point tools can handle a meaningful portion of the intake process without falling over on format variation.

E&S submissions don’t work that way. Broker-specific formats, manuscript endorsements, SOVs in hundreds of variations, loss runs across 400+ carrier formats, handwritten annotations on printed forms, non-standard supplementals with no consistent field structure, all of this arrives in the same inbox and needs to be processed with the same accuracy and speed. A rules-based or template-dependent tool requires the document to conform to an expected pattern. E&S documents routinely don’t.

That complexity is precisely what makes an agentic, workflow-level approach well-suited to this market. Rather than matching documents against predefined templates, an agentic system understands what a document is and what data matters from it, regardless of how it’s formatted. The format variation that breaks other tools is the problem agentic AI handles dynamically.

The economics reinforce the case. MGAs and wholesale brokers typically operate with lean teams relative to the submission volumes they handle. The operational leverage from removing manual intake, the ratio of submissions processed per hour to headcount required, is higher here than in most other parts of the market. For an MGA running high volume with limited administrative capacity, workflow automation addresses the constraint that limits growth most directly.

The Operational Impact

The shift from manual intake to automated workflow infrastructure shows up across several dimensions simultaneously, and the changes compound rather than stack independently.

Turnaround time is the most immediate. Manual submission processing takes anywhere from 40 minutes to several hours, depending on complexity. With a fully automated pipeline, it drops to under one minute. For a team processing hundreds of submissions per week, that compression changes what’s operationally possible.

Throughput scales differently as well. Manual processing is capped by headcount, which means peak periods create backlogs that take days to clear. An automated pipeline processes 1,200 submissions per hour regardless of whether it’s a quiet week or the middle of renewal season. Volume spikes stop being an operational problem and become a manageable variable.

Data quality improves because validation happens at the point of capture rather than downstream. You can catch the errors before they enter the system. The data underwriters work with is cleaner and more complete, which means fewer callbacks to brokers, fewer re-entry cycles, and more reliable inputs into the rating process.

The cumulative effect on underwriting capacity is significant. When the front end of the workflow runs automatically, underwriters spend their time on risk assessment rather than data management. That reallocation doesn’t require adding headcount. The same team handles more submissions, responds to brokers faster, and produces quotes with better underlying data quality, all from removing the manual work that was consuming capacity without contributing to underwriting judgment.

The Competitive Implication

The E&S market is in a softer pricing cycle, and that changes the competitive dynamic in a specific way. When pricing is firm, operational inefficiency is easier to absorb. Margins are wide enough to carry the cost of slow turnaround, manual rework, and submissions that don’t get quoted because the team ran out of capacity. When pricing softens, those inefficiencies become more visible and more consequential.

Global commercial insurance rates fell 5% in Q1 2026, marking the seventh consecutive quarterly decline according to Marsh’s Global Insurance Market Index, and that pricing shift changes the competitive dynamic in a specific way.

Speed to quote is one of the clearest competitive variables in E&S placement. Brokers work with multiple markets simultaneously. The carrier or MGA that responds first with a clean, accurate quote has a structural advantage in winning the placement, and that advantage compounds across a book of business over time. When intake is manual, response time is constrained by how quickly the administrative work in front of underwriting can be completed. When intake is automated, that constraint disappears.

The operational gap between teams that have automated their intake workflow and those that haven’t is already measurable in the market. A national MGA processing 2,000+ submissions per day and responding to brokers five times faster than before isn’t competing on the same terms as one still running manual intake. The difference shows up in bind ratios, broker relationships, and the ability to take on volume growth without the operational strain that typically comes with it.

Workflow automation is moving from a differentiator to a baseline expectation in parts of the E&S market.

What This Looks Like With BoundAI

BoundAI is built specifically for this use case, as a full workflow infrastructure platform for E&S carriers, MGAs, and brokers.

The platform connects submission intake, clearance, policy validation, and distribution into a single structured execution layer that sits inside existing AMS and PAS systems. The full pipeline, classification, extraction, normalization, validation, compliance checks, and downstream integration run automatically. Human review happens for genuine exceptions, items the system flags as low-confidence, rather than items that require manual handling by default.

The operational results from live deployments reflect what that infrastructure delivers. Clients process 1,200 submissions per hour, achieve turnaround times under one minute, capture 250+ data points per submission, and maintain error rates below 1%. Those numbers come from production environments, not controlled demos.

Three integrated platforms make up the full offering. Document AI handles submission intake and clearance, covering every document type that arrives in an E&S inbox across any format without pre-mapping. Document Intelligence covers policy validation between quote and issuance, comparing issued policies against quoted terms and flagging deviations before they reach the book. Broker Workspace structures placement and distribution, connecting carrier marketing workflows, quote normalization, and bind packaging into a single controlled environment.

Deployment happens inside existing infrastructure. There’s no rip-and-replace requirement and no parallel workflow to manage during transition. Implementation typically completes in 8 to 16 weeks, after which the full pipeline runs on the systems the team already uses.

Conclusion

Tools are dominating the AI conversation in E&S insurance. Which ones to evaluate, which ones to buy, which ones are actually ready for production? That’s a reasonable conversation to have, but it misses the more important question, which is what the workflow looks like after automation and whether the operation is actually set up to take advantage of what the technology can do.

Underwriting workflow automation answers that question at the level where it matters. The full chain from submission inbox to AMS entry runs automatically. Underwriters receive structured, cleared, quote-ready files. Volume scales without proportional headcount growth. Data quality improves because validation happens before errors enter the system rather than after.

The E&S market is competitive and getting more so. The teams building automated workflow infrastructure now are creating an operational advantage that compounds over time, in throughput, in turnaround, in broker relationships, and in the ability to grow without the administrative strain that has historically come with it.

For anyone looking to understand what a fully automated underwriting workflow looks like in a live E&S environment, feel free to contact our team.